Unable to Pay Rent, Small Businesses Hope for Deals with Their Landlords

Unable to Pay Rent, Small Businesses Hope for Deals with Their Landlords

ABI Bankruptcy Brief

September 17, 2020

Bankruptcy Brief

NEWS AND ANALYSIS

Unable to Pay Rent, Small Businesses Hope for Deals with Their Landlords

Nearly 98,000 businesses have closed permanently since the pandemic took hold, according to an analysis by Yelp. And the fate of many that remain open increasingly hinges on their ability to renegotiate their leases, the New York Times reported. A recent survey by Alignable, a social network for small-business owners, found that a quarter of those polled had fallen behind on their rent since the shutdowns began. For those in the fitness and beauty industries, the number rose to nearly 40 percent. The problem may worsen now that an initial flood of federal aid has dried up and a sharply divided Congress has been unable to agree on further relief measures. The government’s $525 billion Paycheck Protection Program gave more than 5 million businesses a one-time cash injection to pay workers and other expenses, including rent, but most recipients have now spent the money. Retail rent collections plunged in April to just 54 percent of the total owed, according to Datex Property Solutions, a software company that tracks data on thousands of its clients’ retail properties nationwide. By August, collections had rebounded to nearly 80 percent, but some tenants, like movie theaters, clothing retailers, hair salons and gyms, were much further behind. “When tenants can’t pay the rent, it imperils landlords’ ability to pay their own overhead and their loans, and the whole thing cascades,” Mark Sigal, chief executive of Datex, said.

Fraudsters Steal Millions from Unemployment Coffers, Adding to Pain of Those Still Waiting for Benefits

Over $1 billion in unemployment aid is being threatened by fraud, in schemes ranging from lying about personal income to sophisticated cybercrime, state and federal officials told NBC News. The main target: Pandemic Unemployment Assistance. The widespread fraud is plaguing unemployment systems nationwide, hampering states’ efforts to get money into the right hands. The U.S. Secret Service has launched over 500 investigations in 40 states as part of a multiagency effort to protect taxpayer dollars. “It’s very rampant,” David Smith, the agent in charge of the investigation, said in an interview. “Criminals knew the priority was to get that money into the hands of Americans sooner than later. So they just jumped on an opportunity." In Colorado, cybercriminals took advantage of the unemployment system so aggressively that over the course of one month, 75 percent of applications were ruled fraudulent. In Pennsylvania, thousands of inmates applied and qualified for benefits before getting caught. In California, officials suspect fraud is behind a recent spike of more than 100,000 extra claims. Pandemic Unemployment Assistance was created as part of the Coronavirus Aid, Relief, and Economic Security, or CARES, Act introduced by Congress in March. It provides unemployment benefits to self-employed or gig workers who, in typical circumstances, would not qualify. The program uses federal dollars, but is administered by the states. With almost 7 million people out of work at the start of the pandemic, many states were inundated with a record number of unemployment applications, all while depending on decades-old computer systems. The assistance program is particularly vulnerable because, since it is specifically for self-employed people or independent contractors, there is no employer to verify an applicant’s income. While the CARES Act legislation does ask applicants to submit documents to prove their income, it also allows people to receive the minimum benefit payment of $172 per week without any supporting paperwork.

In related news, the number of Americans applying for jobless benefits resumed its decline, signaling a gradual improvement in the battered labor market, Bloomberg News reported. Jobless claims in regular state programs decreased by 33,000 to 860,000 in the week ended Sept. 12, which coincides with the reference period for the government’s monthly jobs report, according to Labor Department figures released today. Continuing claims, the total number of Americans on state benefit rolls, fell by almost 1 million, to 12.6 million, in the week ended Sept. 5.

Senators Offer Disaster Tax Relief Bill

A bipartisan group of senators yesterday offered legislation to provide tax relief to individuals and businesses affected by natural disasters, such as August's derecho in the Midwest, the wildfires in western states, and Hurricanes Laura and Isaias, The Hill reported. The bill was introduced by Iowa Sens. Joni Ernst (R) and Chuck Grassley (R), California Sen. Dianne Feinstein (D) and Louisiana Sens. Bill Cassidy (R) and John Kennedy (R) — all of whom represent states impacted by disasters in recent months. The bill includes several tax provisions that would apply to individuals and businesses in regions that are designated as presidentially declared disaster areas from July 1 through 60 days after the bill's enactment. It includes provisions to remove penalties on early withdrawal from retirement accounts, suspend limits on deductions for certain charitable contributions and provides an employee retention tax credit. It would also allow low-income individuals to use their previous year's income when claiming certain tax credits, so that they don't receive smaller credits for 2020 if their incomes declined as a result of the disaster.

As Struggling Gas Companies Abandon Wells, Questions About Clean-Up and Environmental Damages Emerge

In the past five years, 207 oil and gas businesses have failed. As natural gas prices crater, the fiscal burden on states forced to plug wells could skyrocket; according to Rystad Energy AS, an industry analytics company, 190 more companies could file for bankruptcy by the end of 2022. Many oil and gas companies are idling their wells by capping them in the hope prices will rise again. But capping lasts only about two decades, and it does nothing to prevent tens of thousands of low-producing wells from becoming orphaned, meaning “there is no associated person or company with any financial connection to and responsibility for the well,” according to California’s Geologic Energy Management Division. “It’s cheaper to idle them than to clean them up,” says Joshua Macey, an assistant professor of law at the University of Chicago, who’s spent years studying fossil fuel bankruptcies. “Once prices increase, they could be profitable to operate again. It gives them a strong reason to not do cleanup now. It’s not orphaned yet, although for all intents and purposes it is.”

White House Suggests Congress Pass Standalone Bill to Help U.S. Airlines

Giving U.S. airlines $25 billion in aid over the next six months could save more than 30,000 jobs, White House Chief of Staff Mark Meadows said today after meeting with the companies’ top executives, suggesting lawmakers approve a separate assistance package for the struggling corporations, Reuters reported. Congress has been deadlocked over approving another round of economic stimulus to blunt the effects of the coronavirus pandemic. But with the first $25 billion in aid to airlines due to run out this month, Meadows said that President Donald Trump would support lawmakers passing a standalone bill to help the companies.

Analysis: Surging Supply of Mortgage-Backed Securities Hasn’t Dampened Investors’ Demand for Them

Low mortgage rates have spurred a boom in home refinancing, which in turn has spurred a boom in the issuance of mortgage-backed securities, the Wall Street Journal reported. The value of single-family mortgage-backed securities issued by Ginnie Mae, Fannie Mae and Freddie Mac totaled almost $322 billion in August, a new monthly record, according to an analysis by industry-research firm Inside Mortgage Finance. Still, the surging supply of mortgage-backed securities hasn’t dampened investors’ demand for them. Yields for the securities have held relatively steady in recent months and even declined slightly, a sign of investors’ continued demand. Much of the demand for mortgage securities comes from the Federal Reserve itself, which said in March it would purchase an essentially unlimited amount of mortgage bonds in an attempt to backstop the credit markets. At its current purchasing rate, the Fed is set to overtake banks as the largest mortgage bond investor, according to Walter Schmidt, senior vice president of mortgage strategies at FHN Financial. (Subscription required.)

In related news, a Mortgage Bankers Association report on Monday found that almost twice the percentage of Ginnie Mae borrowers have demanded forbearance compared to conventional ones, Bloomberg News reported. Mortgages in forbearance have dropped to just over 7 percent of the overall universe, the lowest since April. However, Ginnie Mae has a higher share of those - 9.1 percent versus 4.6 percent for conventional mortgages backed by Fannie Mae and Freddie Mac, the MBA data show. The average FICO score for the Ginnie Mae II 30-year borrower is 705, whereas for the conventional 30-year borrower it’s 758. When borrowers fall into forbearance and delinquency, this heightens the risk that the loan will eventually go into default and need a buyout, which for mortgage investors are prepayments by another name as it will be bought out at par. This can weigh on portfolio performance. While the percentage of Ginnie Mae homeowners in forbearance did drop by 50 basis points in the latest report, “at least a portion of the decline in the Ginnie Mae share was due to servicers buying delinquent loans out of pools and placing them on their portfolios,“ said Mike Fratantoni, the MBA’s senior vice president and chief economist. The trend may get worse for Ginnie Mae MBS investors before it gets better. “Forbearance requests increased over the week, particularly for Ginnie Mae loans,” Fratantoni said. “With just under 1 million unemployment insurance claims still being filed every week, the lack of additional fiscal support for the unemployed could lead to even higher increases of those needing forbearance.”

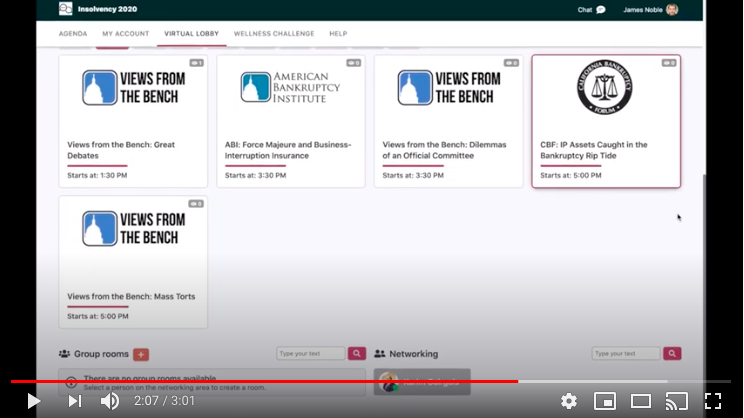

ABI Sessions Next Week at Insolvency 2020 Summit: Great Debates, Force Majeure and Business Insurance and Dilemmas of an Official Committee

Sept. 23

• Views from the Bench: Great Debates

• Force Majeure and Business-Interruption Insurance

• Views from the Bench: Dilemmas of an Official Committee

• Views from the Bench: Mass Torts

Sept. 24 • Views from the Bench: Sales — Chapter 11 or § 363?

• Views from the Bench: Confirmation Roundtables: Competing Interests in Today's Chapter 11

Sixteen leading insolvency organizations are participating in the Virtual Summit through Oct. 27 to bring thought leaders from the worlds of restructuring, insolvency and distressed debt for insightful online programming and engaging networking via a state-of-the-art virtual platform. Click below to learn more about how the Insolvency 2020 platform provides attendees with an enhanced online conference experience:

Sign up Today to Receive Rochelle’s Daily Wire by E-mail!

Have you signed up for Rochelle’s Daily Wire in the ABI Newsroom? Receive Bill Rochelle’s exclusive perspectives and analyses of important case decisions via e-mail!

New on ABI’s Bankruptcy Blog Exchange: Pandemic Threatens to Stifle Bank M&A for Another Year

With data privacy issues constantly in the news, a recent blog post looked at what businesses need to know about handling personal information when they’re considering bankruptcy, especially if some personal information — like customer records — may be a valuable asset.

To read more on this blog and all others on the ABI Blog Exchange, please click here.