Report: U.S., Canadian Oil Company Bankruptcies Surge 50 Percent in 2019

Report: U.S., Canadian Oil Company Bankruptcies Surge 50 Percent in 2019

ABI Bankruptcy Brief

January 23, 2020

Bankruptcy Brief

NEWS AND ANALYSIS

Report: U.S., Canadian Oil Company Bankruptcies Surge 50 Percent in 2019

A report released yesterday by Dallas law firm Haynes and Boone said that the number of oil and gas company bankruptcies in the U.S. and Canada increased 50 percent in 2019 over the previous year, and is likely to increase as a slide in energy prices continues to shake producers, Reuters reported. U.S. and Canadian oil and natural gas exploration and production company bankruptcies totaled 42 in 2019, up from 28 in 2018, the law firm said. A total of 208 oil and gas production companies filed for bankruptcy between 2015 and 2019, according to the report. "This increase in year-over-year filings indicates that the reverberations of the 2015 oil price crash will continue to be felt in the industry through at least the first half of 2020," Haynes and Boone said in the report. Oilfield service companies were again hit hard with the number of bankruptcies nearly doubling from 12 in 2018 to 21 in 2019, the largest being the $7.4 billion filing by Weatherford International in July. Midstream companies that provide storage and pipelines to producers fared better, with only two bankruptcies in 2019 out of a total of 28 since the beginning of 2015.

U.S. Regulator to Move on Low-Income Lending Overhaul Without Fed

A top U.S. banking regulator said yesterday that he plans to push ahead with a proposal to overhaul rules governing billions of dollars of lending in low-income neighborhoods despite objections from the Federal Reserve, the Wall Street Journal reported. Comptroller of the Currency Joseph Otting said that he doesn’t see that there is time to compromise with the Fed regarding a December proposal that would update federal regulations under the Community Reinvestment Act. The proposal was crafted jointly by his office and the Federal Deposit Insurance Corp. Otting said that the Office of the Comptroller of the Currency will receive comments on its proposal until March 9 and issue a final rule about 60 days later. The growing rift among federal banking regulators makes it likelier that banks will have to navigate different sets of rules under the community reinvestment law, which was enacted in 1977 to end “redlining” — the practice of avoiding lending in certain areas, often lower-income communities, which served to deepen racial disparities in housing and education. The OCC oversees roughly 70 percent of activity under the rules, and its proposal would apply to some 1,200 banks — including some of the biggest, such as JPMorgan Chase & Co. and Wells Fargo & Co. The Fed oversees about 15 percent of CRA activity. Earlier this month, Fed governor Lael Brainard, who is leading the central bank’s efforts to update the act, criticized the joint proposal by the OCC and FDIC. She said that it could encourage some banks to meet their CRA requirements through a small number of large loans or investments, potentially reducing many poor and middle-class Americans’ access to financing. (Subscription required.)

110 Million Consumers Could See Their Credit Scores Change Under New FICO Scoring

Americans who are struggling to pay off their debt could see lower FICO credit scores in their future, especially if they miss payments, CNBC.com reported. Fair Isaac Corp., the company behind the popular FICO credit score, announced the launch of its latest FICO 10 model today, Jan. 23, that will start incorporating consumers’ debt levels into their scoring model. This comes as total household debt in the U.S. has steadily increased for about two years, and currently sits at about $13.95 trillion as of September 2019, according to the Federal Reserve Bank of New York. That’s higher than the previous high of $12.68 trillion seen right before the 2008 financial crisis. FICO estimates that about 110 million consumers will see a change to their score under the new credit score model, with most people seeing less than a 20-point swing in either direction. Roughly 40 million will see a shift upward over 20 points and another 40 million will see a shift downward, FICO says. The new scoring model will also likely create a wider gap between those who are considered good credit risks and those who are not. Consumers who already have good credit, for example, and who continue to whittle down their existing loans and make on-time payments will see higher scores. But those who score below 600 will see bigger dips in their scores under the new model.

Commentary: Chicago Doubling Down on Dangerous ‘Securitized Bonds'

Chicago's already sold off its share of future sales tax revenue that flows from the state to secure other bonds, and new bondholders will be taking a junior ownership position in that, according to a Crain's Chicago Business commentary. The city indeed will get about $250 million up front, from refunding savings, to put toward this year's budget. The exact numbers on that and some other aspects of the new bond offerings were still pending as this was being written. While chances may be remote that Chicago would go bankrupt, bond buyers are not that optimistic. That's why they want conveyance of full ownership of streams of income to collateralize their loans, called "securitized bonds." Prevailing legal opinion says they are likely, though not entirely certain, to get priority for payment over everything else, even in bankruptcy. The big losers may end up being taxpayers, service recipients, public pensioners and everybody else with a stake in government except the muni bond community: bondholders, underwriters, bankers, lawyers and so on, according to the commentary. Securitized bonds raise the risk of an "assetless bankruptcy," the worst of all outcomes. The debtor then has nothing to work with to get a fresh start, and there's nothing left for unsecured creditors. Those unsecured creditors would include pensioners insofar as pensions are underfunded.

Shadow Banks Come into the Light in Global Lending

According to Bank for International Settlements data released this week, nonbank financial institutions are leading the growth in cross-border lending, with cross-border banking claims in the third quarter up 17 percent from a year earlier. That’s the fastest growth in at least six years, when records began, the Wall Street Journal reported. Banks’ cross-border claims on and liabilities to nonbank financiers have risen by nearly $8 trillion since the end of 2013, while their cross-border exposure to other banks has actually declined slightly under the weight of increasingly stringent regulations. Shadow banks typically include brokers, clearinghouses, funds, investment trusts and structured finance vehicles. While there is nothing inherently wrong about their becoming more important, the shift raises questions among experts about how they’ll behave in a sharp slowdown or financial crisis. (Subscription required.)

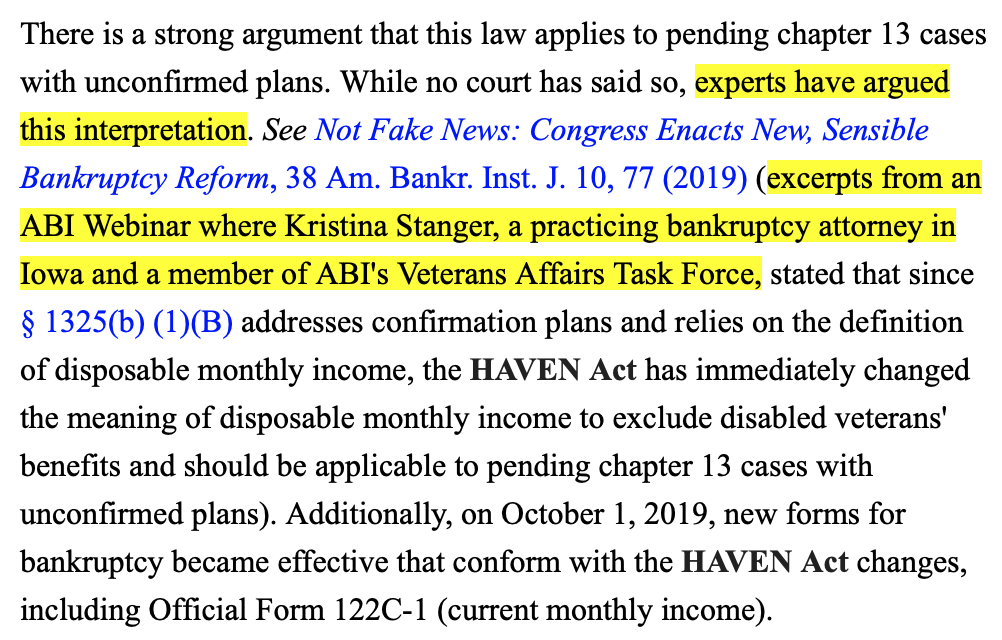

First Published Opinion on Retroactive Application of the HAVEN Act References ABI's Veterans Affairs Task Force

Hon. Robert Jones of the U.S. Bankruptcy Court for the Northern District of Texas provides good supporting authority in a Nov. 21, 2019, dicta opinion for the retroactive application of the HAVEN Act to cases that were pending when the President signed the bill into law on Aug. 23, 2019. The In re Price opinion is also notable for its reference to ABI's Veterans Affairs Task Force. See below:

Sign up Today to Receive Rochelle’s Daily Wire by E-mail!

Have you signed up for Rochelle’s Daily Wire in the ABI Newsroom? Receive Bill Rochelle’s exclusive perspectives and analyses of important case decisions via e-mail!

New on ABI’s Bankruptcy Blog Exchange: Denial of Stay Relief Is a Final Order, Says the U.S. Supreme Court

The Supreme Court in Ritzen Group Inc. v. Jackson Masonry LLC issued a unanimous opinion last week, ruling that the Sixth Circuit Court of Appeals correctly denied the ability of creditor Ritzen Group Inc. to appeal the bankruptcy court’s order denying as untimely Ritzen’s motion for relief from the automatic stay in Jackson Masonry’s chapter 11 case, according to a recent blog post.